As we have now entered the February reporting season (July to December ½) for publicly listed companies we thought it worth sharing some views. For this financial year analysts’ remain of the view that overall company earnings growth for the ASX 200 (largest 200 groups) will be circa 18% which is mainly coming from the recovery in commodity prices and hence the significant pick up in earnings for mining groups such as BHP and Rio Tinto. Outside of the mining sector the typical company is expected to deliver approximately 5% growth in earnings for the current year. Global factors such as commodity price moves, US Dollar vs AU Dollar, US economic growth will continue to deliver the greatest impetus for upgrades to the domestic earnings outlook. Growth stocks have over the past three to six months seen some setbacks to their outlook and where they have been priced for perfection some have seen some rerating of their share prices. Such growth stocks will be a key focus during the reporting season to see if they still deserve to be priced even at current price to earnings multiples and are providing a more realistic outlook for the six months ahead. Well-known companies due to release results during February including day of release are Rio Tinto (8thFebruary), AMP (9th), JB Hi Fi (13th..many analysts’ expecting the discretionary retailers such as Harvey Norman and Super Retail Group to do well), Commonwealth Bank (15th), Wesfarmers (Coles and Bunnings, 15th), Telstra (16th), Medibank (17th), BHP (21st), Woolworths (22nd) and Qantas (23rd).

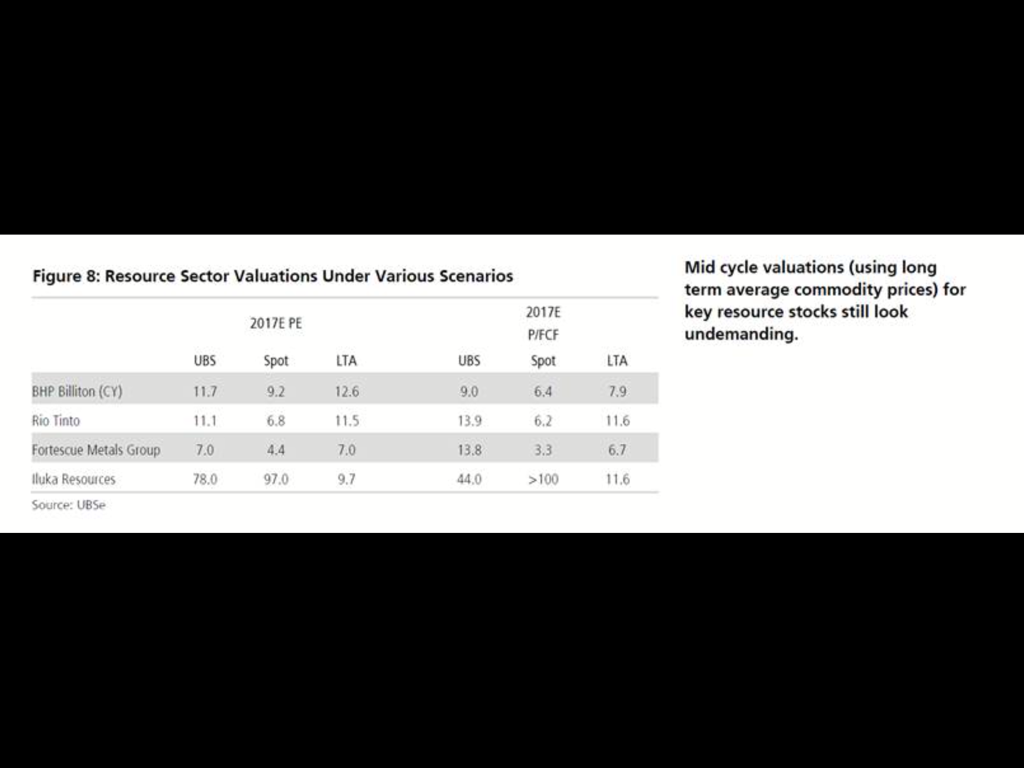

Overall the outlook remains that most investors should have a pro-cyclical bias within their share investments i.e. resources (companies still not reflecting pick up in commodity prices on historical valuations. See below table), banks as their yield curve (longer term rates) continue to steepen so will banks margins and the industrial sector should see a greater reliance on the January to June profit half unfortunately being aided by no great moves in the Australian dollar. As we move further through the calendar year (and maybe reflected in this reporting season) the focus is expected to move away from the international focus to being more domestic (see recent strong +ve bounce in the NAB business survey) as the period of uncertainty surrounding US policy increases (protectionism over tax and infrastructure stimulus) and potential that the improving global growth starts to fade (started well before Trump and November 9).

Resource company valuations versus longer term scenario:

Overall the outlook remains that most investors should have a pro-cyclical bias within their share investments i.e. resources (companies still not reflecting pick up in commodity prices on historical valuations. See below table), banks as their yield curve (longer term rates) continue to steepen so will banks margins and the industrial sector should see a greater reliance on the January to June profit half unfortunately being aided by no great moves in the Australian dollar. As we move further through the calendar year (and maybe reflected in this reporting season) the focus is expected to move away from the international focus to being more domestic (see recent strong +ve bounce in the NAB business survey) as the period of uncertainty surrounding US policy increases (protectionism over tax and infrastructure stimulus) and potential that the improving global growth starts to fade (started well before Trump and November 9).

Resource company valuations versus longer term scenario:

Consensus earnings revisions over past 3-12 months shows that the current earnings upgrade cycle is being dominated largely by the areas of mining, health care and consumer staple

As we move through reporting season and themes are worth discussing (company or sector or market as a whole) we bring this information to you.

Marcus Pringle-Jones

Client Adviser.

Bell Potter Securities Limited

Ph: (03) 6281 6206 | M: 0413 164 674

E: [email protected]

Lvl 9, NAB Building, 86 Collins Street, Hobart TAS

GPO Box 310, Hobart TAS 7001

Marcus Pringle-Jones

Client Adviser.

Bell Potter Securities Limited

Ph: (03) 6281 6206 | M: 0413 164 674

E: [email protected]

Lvl 9, NAB Building, 86 Collins Street, Hobart TAS

GPO Box 310, Hobart TAS 7001

RSS Feed

RSS Feed